An RV loan payoff calculator with depreciation is one of the most vital financial tools for anyone preparing to buy, own, or deal with an unpaid vehicle. Many mass-market focus only on the excitement, comfort, and freedom that come with RV ownership, but the fiscal benefits are often overlooked. An RV isn’t just a vehicle; it’s a large, depreciating asset that can affect your finances for many years. Understanding the manner in which your loan balance and your RV’s value change over time can shelter you from costly mistakes and unexpected losses.

Because most buyers finance an RV, they commit to a long-term loan that may last 10 to 20 years. These long loan terms are attractive because they reduce monthly payments, making the RV seem affordable. Then again, this affordability is ofttimes misleading. While your lending correspondence decreases slowly in the early years, the worth of your RV drops rapidly. Without considering depreciation, many buyers believe they’re making progress when, in reality, they may be sinking deeper into negative equity.

How the Math Works

If you plan to write an article explaining this to your readers, there are two distinct calculations happening simultaneously behind the scenes.

1. Loan Amortisation

The calculator calculates exactly how much principal remains on the loan using the standard mortgage amortization formula. If a user is $k$ months into an $n$-month loan, the remaining balance ($B_k$) on the principal ($P$) at a monthly interest rate ($r$) is calculated as:

2. RV Depreciation

Unlike a house, an RV loses value over time. The calculator uses a “declining balance” depreciation method (an approach where the RV loses a set percentage of its value each year). If the RV depreciates by an annual rate ($d$), its value after a certain number of months ($k$) based on its original value ($V_0$) is:

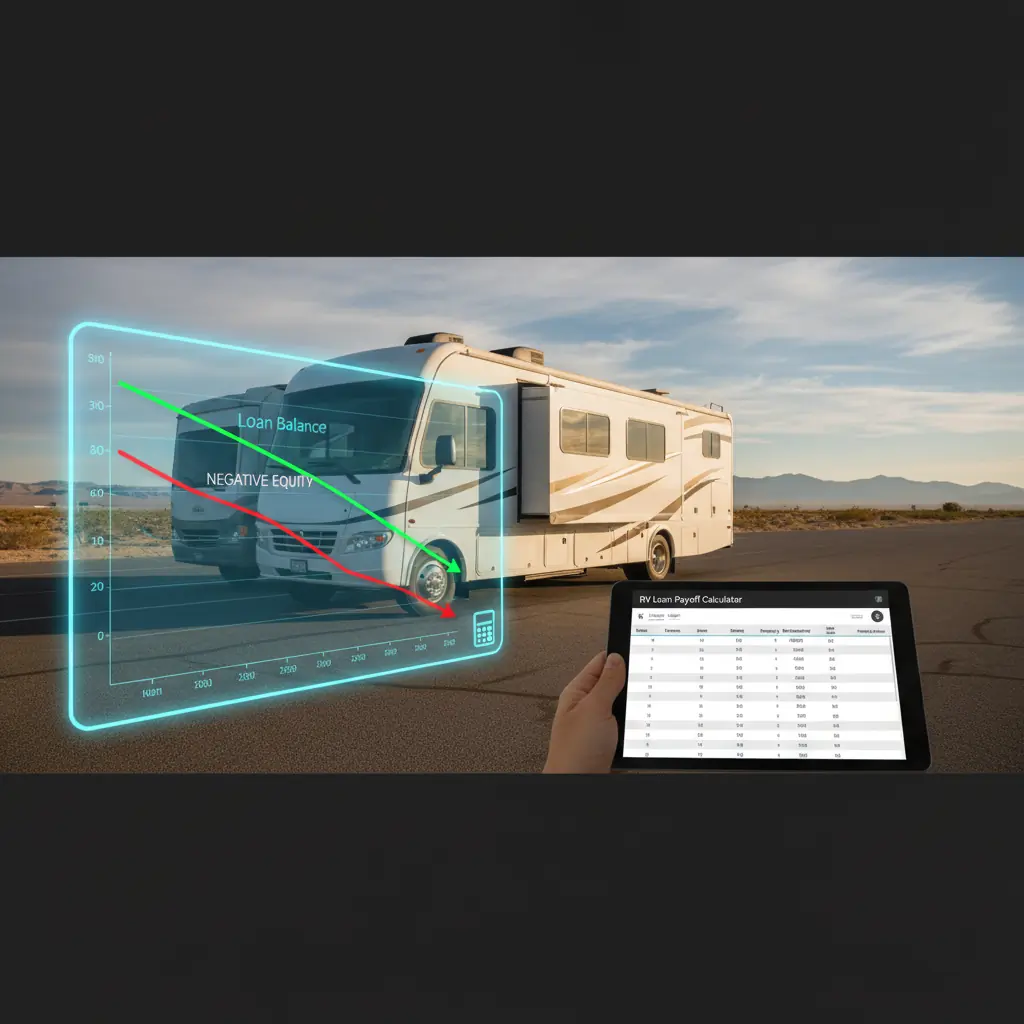

By subtracting the remaining loan balance from the current estimated value, the calculator reveals the user’s equity (the difference between what you owe and what the RV is worth). If the box turns red, it means the owner is “underwater,” owing the bank more than the vehicle is currently worth.

Understanding RV Depreciation and Loan Amortization

Disparagement is the silent cost of RV possession. The moment a fresh RV is driven off the lot, its market significance drops significantly. Often, an RV can lose 20 to 30 percent of its value in a low year. Over the next few years, the value continues to decline, though at a slightly slower pace. By the time an RV is five years old, it may be worth only half its original price, even if it has been well-maintained. This rapid decline in importance makes RV financing particularly risky compared to other purchases.

An RV loan payoff calculator helps you see how your loan balance changes month by month. It shows the method by which much of your payment goes toward interest and the manner in which much goes toward reducing the principal. In the crude years of a long loan, an important portion of your payment goes to interest, which means your actual debt decreases immensely slowly. This is what many owners are surprised by. They make regular payments for years, yet still owe nearly as much as they did when they started.

As soon as depreciation is superimposed on the payoff calculating machine, the picture becomes much clearer. A reckoner that includes disparagement compares two weighty curves over time: the declining loan correspondence and the declining benefit of the RV. By looking at both together, you can immediately see whether you’re building equity or falling behind. This comparison is critical because it reveals the owner’s true financial position at any given point in the loan term.

Managing Negative Equity and Extra Payments

Negative equity is one of the biggest risks in RV possession. If you decide to sell the RV, the sale price won’t be reasonable to pay off the loan, as being underwater on a loan means that. This can happen for many reasons, like job changes, health issues, or simply realizing that RV life isn’t what you expected. When negative equity exists, selling the RV requires extra cash to cover the remaining loan balance, which can be financially stressful.

An RV loanword issue reckoner with wear and tear helps avoid this state by screening the technique for long negative equity that is likely to last. Often, owners don’t reach positive equity until several years into the loan term, especially if the down payment was small. Seeing this timeline in advance allows buyers to make smarter decisions, like increasing the down payment, choosing a shorter loan term, or providing extra payments crude in the loan.

Extra payments can have a potent effect on both loan payoff and equity. Even petty additional monthly payments can significantly shrink the principal equilibrium over time. The moment that the principal decreases faster, interest costs drop, and the loan counterbalance begins to fall below the RV’s worth sooner. A calculating machine that includes wear and tear allows you to test different extra payment amounts and see exactly how the system changes your fiscal trajectory.

The Impact of Down Payments, Loan Terms, and Refinancing

The size of the blue payment plays a vital role in managing disparagement. A larger down payment reduces the initial loan share, providing a buffer against the sharp drop in benefits in the first year. You who put very little down are almost guaranteed to be underwater on crude. By using an RV loan yield calculator with wear and tear, you can compare scenarios and understand how much dispirited payment is needed to stay financially protected.

Lend term length is another critical aspect. Longer price shrink monthly payments, then again elevate the total interest paid and extend the time of negative equity. Shorter footing raises monthly payments but builds equity faster and lowers boiler suit costs. Many buyers choose long-term damage without realizing the long-term consequences. A depreciation-aware calculator makes these trade-offs visible and easier to rate.

Refinancing is sometimes considered as a way to reduce interest rates or monthly payments. Then again, refinancing an RV loan can be challenging if the RV has depreciated significantly. Lenders may need the loan equilibrium to be close to or below the RV’s current weight. By tracking depreciation alongside loan yield, you can determine whether refinancing is realistic and if it’ll truly improve your financial position.

Selling, Budgeting, and New vs. Used RVs

Selling or trading in an RV is another stage at which depreciation awareness is essential. Many owners are shocked when they acquire trade-in offers that are far below their remaining loan balance. This shock stems from years of focusing on monthly payments rather than overall weight. Exploitation of a payoff computer with disparagement before making a decision to deal allows you to plan the timing and avoid unpleasant surprises.

Budgeting for RV ownership becomes much more rigorous once depreciation is included. Loan payments are only one part of the cost. Sustenance, insurance, storage, fuel, and campsite fees all add up. While derogation is in place, you see the full annual cost of possession. If RV possession truly fits your modus vivendi and financial goals, this realistic budgeting helps identify whether it matters.

We also have a major divide between buying a new RV and a used one. Original RVs depreciate the most in the first year. Used RVs, as they are not immune to depreciation, have already absorbed much of the initial importance loss. A reckoner that includes depreciation allows buyers to compare new and used options fairly, screening for the method by which lower depreciation can offset higher interest rates on used RV loans.

The Psychological and Practical Benefits for Current Owners

Many RV buyers make the mistake of basing their provisions on optimism rather than on numbers. They suppose they’ll keep the RV for decades or that the resale value will be higher than anticipated. Real-world circumstances change a great deal. A fiscal drive that accounts for depreciation introduces realism into the decision-making routine, which is more protective than optimism alone.

An RV loan payoff estimator with depreciation isn’t just for buyers. Current RV owners can also benefit from victimization one. By entering current loan details and an estimated RV merit, owners can assess whether making extra payments, refinancing, or even selling makes sense. This ongoing awareness allows for proactive fiscal direction rather than reactive decision-making.

The psychological advantage of perceiving your fiscal position shouldn’t be underestimated. Uncertainty about debt and benefits can cause stress and limit the enjoyment of RV ownership. While you know exactly where you stand and what to expect, you can focus more on the history and less on financial worry. Clarity brings confidence, and confidence enhances enjoyment.

Conclusion

Using such a figure effectively requires honest inputs. Overestimating resale benefit or underestimating derogation can lead to false comfort. It is better to use conservative assumptions and be pleasantly surprised than to depend on optimistic estimates that may not materialize. Exploring multiple scenarios provides a more holistic understanding of doable outcomes.

In the end, an RV loan payoff calculator that accounts for wear and tear reveals the true cost of owning an RV. It shows that affordability isn’t just about monthly payments but about long-term financial health. By combining loanword amortization with realistic value decline, this tool empowers buyers and owners to make informed, responsible decisions.

RV ownership can be a rewarding and fulfilling experience when approached with fiscal awareness. By understanding how loans and disparagement interact, you can avoid common pitfalls, protect your investment, and enjoy the journey with peace of mind. A calculator that includes derogation isn’t just a helpful characteristic; it’s a crucial companion for anyone earnest about owning an RV responsibly.